Needs vs. Wants: The Secret to Saving More Money

Effective money management begins with a simple yet powerful concept: distinguishing between needs and wants. Understanding this difference is foundational for anyone seeking to build savings, reduce debt, and achieve long-term financial stability. By learning to prioritize necessities over desires, you can unlock the secret to saving more money and avoiding impulsive spending traps.

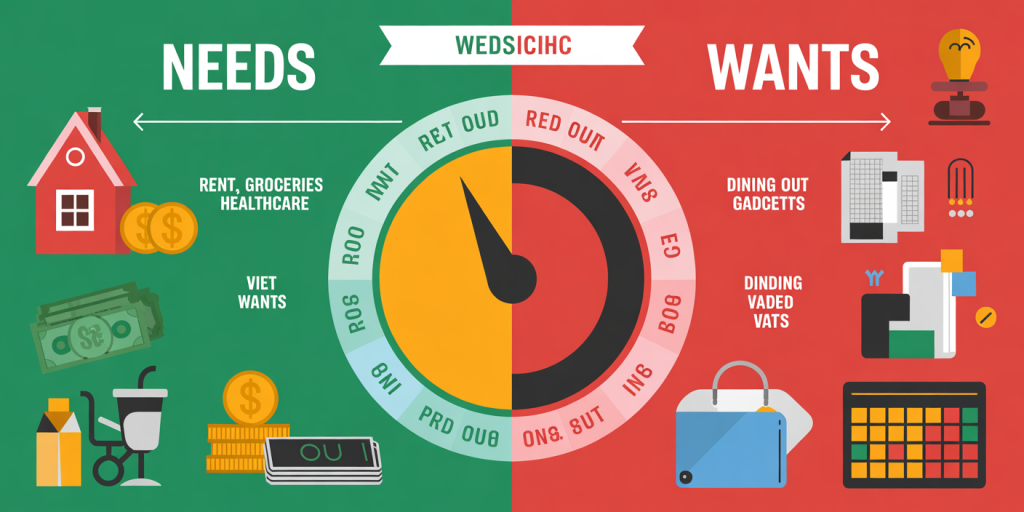

The Psychological Foundation of Needs and Wants

Spending behaviors are often driven by emotional impulses rather than logical assessments. Needs are basic requirements essential for survival and well-being, such as food, housing, healthcare, and clothing. Wants, by contrast, are non-essential items that enhance comfort or satisfaction, such as luxury gadgets, dining out, or vacations.

According to a 2023 study by the National Endowment for Financial Education (NEFE), nearly 60% of adults struggle with differentiating needs from wants, often leading to unnecessary spending. This blurring line results in diminished savings and increased reliance on credit. Behavioral economists suggest that consumers can benefit from cognitive reframing—thinking of “wants” as future rewards after satisfying “needs” first, fostering disciplined expenditure.

Categorizing Expenses: Practical Examples

Anúncios

One of the most effective ways to start saving more is to create a clear breakdown of monthly expenses into ‘needs’ and ‘wants.’ For instance, consider Jane, a 30-year-old professional whose monthly expenses total $3,500. Her rent, groceries, utilities, and insurance add up to $2,100—her needs. Meanwhile, her subscriptions, dining out, and entertainment cost $1,400, representing wants.

Anúncios

| Expense Category | Description | Monthly Cost | Classification |

|---|---|---|---|

| Rent | Apartment lease | $1,200 | Need |

| Groceries | Food and essentials | $400 | Need |

| Utilities | Electricity, water, internet | $300 | Need |

| Insurance | Health and auto insurance | $200 | Need |

| Dining Out | Restaurants, cafes | $600 | Want |

| Entertainment | Movies, events, streaming | $500 | Want |

| Subscriptions | Gym, magazines, apps | $300 | Want |

From this breakdown, Jane reviewed her budgets to minimize wants, reducing dining out by $300 and canceling one unused subscription, saving $350 monthly. This small adjustment freed up $650, which she redirected toward savings and debt repayment.

The Impact of Prioritizing Needs Over Wants on Savings

Reallocating money from wants to needs or savings has profound financial implications. Data from the Bureau of Economic Analysis (BEA) in 2022 reported that Americans spend approximately 20% of their disposable income on non-essential items. For an average household with a median income of $70,000, that equates to $14,000 annually.

By consciously cutting down wants by only half (10% of income), a family could potentially save $7,000 a year. Over a decade, accounting for compound interest from a typical savings account with a 2% interest rate, this accumulates to approximately $77,000—a significant nest egg for emergencies or investments.

Case studies from debt counseling services illustrate how this mindful budgeting approach reverses financial distress. One client, a family of four, initially spent 35% of their monthly income on wants. After implementing needs-first budgeting, they reduced want expenses to 15%, cleared $10,000 in credit card balances in six months, and started contributing regularly to a college fund.

Tools and Techniques for Differentiation and Control

Budgeting apps and financial literacy programs emphasize the following methods to help distinguish needs from wants: The 50/30/20 Rule: Suggests allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment. The Delay Tactic: Encourages waiting 48 hours before making a non-essential purchase to avoid impulse spending. Envelope System: Physically or digitally segregating money for needs and wants, preventing overspending in either category.

For example, Mike and Sarah started using the envelope system, allocating $800 monthly for wants and $1,500 for needs. Initially, their wants envelope ran out by the 20th of each month, but conscious spending improved gradually, increasing their monthly savings by $500 in just four months.

Financial advisors also recommend periodic reviews of spending categories, as what qualifies as a need or want may evolve over time due to lifestyle changes or economic conditions. This adaptability ensures that financial goals remain aligned with personal circumstances.

Real-Life Success Stories: From Spending Traps to Savings Growth

There are numerous documented cases where the clear distinction between needs and wants transformed financial health. A popular example is Sarah Stanley, author of a bestselling personal finance book, who paid off $25,000 in student loans within two years by strictly minimizing wants.

She detailed her strategy of cooking meals instead of eating out, using public transportation rather than owning a car, and delaying any luxury purchases until her debt was cleared. This discipline allowed her to save over $300 monthly, leading to quicker loan repayments and reduced interest expenses.

Similarly, a 2021 survey by the Financial Times revealed that 47% of respondents who practiced needs-focused budgeting saw their savings increase by at least 20% within one year. The key takeaway was the empowerment gained by making intentional spending decisions, enhancing both financial stability and psychological satisfaction.

Comparative Overview: Needs Versus Wants Impact on Long-Term Financial Goals

| Aspect | Needs | Wants | Impact on Savings and Financial Goals |

|---|---|---|---|

| Definition | Essential for survival and daily function | Non-essential, enjoyment-based | Needs fulfillment is non-negotiable; wants are discretionary |

| Examples | Rent, groceries, healthcare | Dining out, vacations, gadgets | Prioritizing needs preserves financial foundation |

| Flexibility | Generally fixed or non-negotiable | Highly flexible | Wants can be adjusted to increase savings |

| Emotional Influence | Less influenced by impulse, necessity driven | Highly prone to impulse and desire | Managing wants requires self-control |

| Long-Term Financial Impact | Supports stability and security | Can deplete funds if unchecked | Neglecting needs risks hardship; prioritizing wants risks savings |

| Savings Potential | Limited scope (must be covered) | High potential for savings reduction | Cutting wants directly boosts savings |

This comparative table highlights that while needs are non-negotiable expenses, wants provide ample room for adjustment and cost-cutting, essential for achieving financial goals like emergency funds, investments, or retirement savings.

Looking Ahead: The Future of Financial Discipline Through Needs vs. Wants

In an era of increasing consumerism supported by digital marketing, subscription services, and easy credit, distinguishing needs from wants will become more critical. Emerging technologies like artificial intelligence-driven financial planners and smart spending trackers can help individuals make these fine distinctions with more precision.

Moreover, financial education focusing on this core concept is gaining momentum in schools and workplaces, aiming to instill lifelong money management skills early on. As younger generations face economic uncertainties such as inflation and housing affordability challenges, their ability to control discretionary spending will directly affect their resilience.

Policies encouraging transparency in marketing and promoting savings incentives tied to responsible spending patterns may also emerge. This could involve tax benefits or interest rate bonuses for individuals who demonstrate effective budgeting that prioritizes needs.

On a personal level, cultivating mindfulness around consumption habits—recognizing emotional triggers versus genuine necessity—will remain a cornerstone of financial wellness strategies. By fostering a culture of intentional spending, the secret to saving more money through needs versus wants can become attainable for a broader population.