How to Create and Maintain Healthy Habits That Improve Your Financial Life

In today’s fast-paced world, financial stability often hinges on the small, consistent habits individuals cultivate over time. While many people strive for wealth and economic security, the key to achieving these goals often lies not in grand gestures or sudden windfalls but in the development of healthy financial habits. These habits shape behavior, influence decision-making, and ultimately determine financial well-being in the long run.

Understanding how to create and maintain these habits is crucial for anyone looking to improve their financial life. This article explores practical strategies backed by data, real-world examples, and expert insights to help you build habits that foster savings, reduce debt, and enhance overall financial health. By the end of this discussion, you’ll be equipped to take steady, effective steps toward financial empowerment.

The Psychology Behind Financial Habits: Why Consistency Matters

Before diving into specific habits, it’s important to understand why habits form and how consistency reinforces them. Financial habits, like any others, rely on a cue-routine-reward loop. A cue triggers a behavior (routine), which then delivers a reward, making the loop self-reinforcing. For example, receiving your paycheck could be a cue to review your budget (routine), which provides the reward of financial clarity or control.

Anúncios

A 2018 study by the University College London revealed that it takes an average of 66 days to form a new habit, highlighting the need for persistence. Applied to finance, this means regularly setting time aside for money management or making deliberate choices like transferring funds into a savings account can eventually become automatic behaviors that protect and grow your financial health.

Moreover, behavioral economics specialists suggest breaking down larger financial goals into smaller, manageable actions. This approach combats “present bias,” where individuals prioritize immediate gratification over long-term benefits. By automating small, regular financial decisions—such as saving $20 weekly—people reduce the mental friction around money management and build sustainable habits.

Building the Foundation: Budgeting and Expense Tracking

One of the most fundamental steps to improving financial health is gaining clarity on income and expenses. Budgeting and expense tracking provide this clarity, revealing habits that can be adjusted for better money management. According to a 2023 survey by the National Endowment for Financial Education, individuals who regularly track expenses are 30% more likely to report financial satisfaction than those who don’t.

Starting with a budget doesn’t require complex software; even a simple spreadsheet or budgeting app like Mint or YNAB can suffice. The critical habit is consistency—setting aside 10-15 minutes weekly to review all transactions and compare them with budgeted limits. Over time, this habit helps identify unnecessary expenditures and frees up cash flow for savings or debt repayment.

For instance, consider the case of Amanda, a 29-year-old graphic designer who once ignored her spending habits. After adopting weekly budget reviews, she noticed frequent dining-out expenses that added up to nearly $200 monthly. By cutting back and preparing meals at home, Amanda redirected that money to her emergency fund, increasing her financial security. This example underlines how habitual expense monitoring leads to actionable insights and tangible financial improvements.

Anúncios

| Habit | Benefit | Tools/Examples |

|---|---|---|

| Weekly expense tracking | Greater financial awareness | Mint, YNAB, Excel spreadsheets |

| Automated budgeting reminders | Consistency in budget reviews | Calendar alerts, app notifications |

Saving Smart: Automate and Prioritize Your Financial Goals

Habitual saving is one of the most impactful behaviors for financial improvement. However, merely intending to save is often insufficient due to procrastination or competing priorities. Creating an automated system removes the reliance on willpower and promotes consistency.

Studies from the Federal Reserve indicate that as of 2022, only 39% of Americans have automated transfers to savings accounts despite evidence that autopay setups increase savings rates by 40%. Setting up automated recurring transfers immediately after each paycheck ensures money is consistently directed towards savings before discretionary spending occurs.

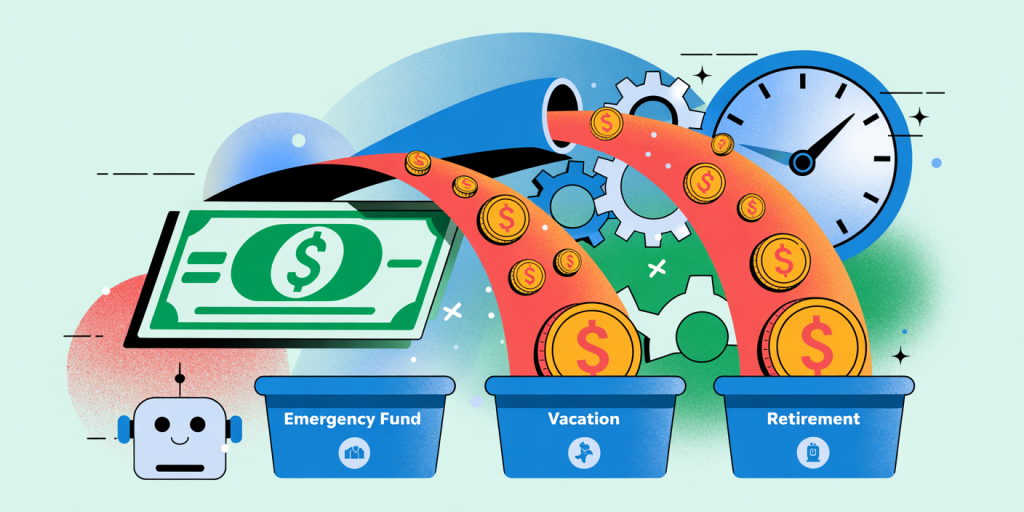

Prioritizing savings goals is equally important. Creating categorized savings (for an emergency fund, vacation, retirement) helps maintain focus and motivates regular contributions. For example, a study by Bankrate.com found that individuals with targeted savings accounts were 25% more likely to adhere to their saving plans.

A practical example is Michael, an engineer who wished to build an emergency fund but found it challenging to save manually. After establishing a $200 automatic transfer every payday, his savings grew steadily without impacting daily spending habits. Setting clear goals and automating contributions transformed saving from a vague intention into a reliable habit.

Debt Management: Creating Healthy Repayment Rituals

Debt management is a crucial dimension of financial health. High-interest debt, such as credit cards, can quickly sabotage financial goals if left unchecked. Establishing habits around debt repayment can significantly reduce financial stress and increase net worth.

Key habits include prioritizing debts using a method like the “debt avalanche” (paying higher-interest debts first) or the “debt snowball” (paying the smallest debts first to boost motivation). According to a 2021 study published by the Journal of Consumer Research, the debt snowball method increases psychological motivation, with 35% more people completing debt repayment plans compared to other methods.

Creating a ritual—such as reviewing debt balances and payment schedules every Sunday—instills discipline and helps allocate extra income toward debt. Real-life cases confirm this: Jennifer, a schoolteacher, faced $12,000 in credit card debt. By reviewing her debts weekly and making targeted payments, she became debt-free in two years, despite modest earnings.

| Debt Repayment Method | Psychological Benefit | Recommended Use Case |

|---|---|---|

| Debt Avalanche | Saves more interest, logical | For those prioritizing cost efficiency |

| Debt Snowball | Motivational, small wins | For individuals needing frequent progress |

Investing in Financial Education: Cultivate Lifelong Learning

Maintaining a healthy financial life extends beyond managing money day-to-day; it also requires continuous education. Financial literacy enables informed decisions about investments, taxes, insurance, and retirement planning, areas that can significantly amplify wealth.

Creating habits like subscribing to reputable financial newsletters, reading one finance book per quarter, or attending workshops help build and update financial knowledge. The FINRA Investor Education Foundation reports that financially literate individuals are twice as likely to plan for retirement and have a diversified investment portfolio.

Take the case of Robert, who initially had zero investment knowledge. By dedicating 20 minutes daily to learning through podcasts and online courses, he gradually shifted from a cash-only mindset to investing in index funds and retirement accounts. His growing knowledge enabled better risk assessment and portfolio diversification, ultimately improving his financial resilience.

Leveraging Technology: Tools That Support Healthy Financial Habits

In today’s digital era, technology offers numerous tools to create and maintain financial habits. From budgeting apps and robo-advisors to credit score trackers, technology streamlines money management, making it more accessible and actionable.

For instance, apps like Personal Capital provide comprehensive views of net worth and investment performance, while credit monitoring services like Credit Karma alert users of changes that could impact loan eligibility. Setting up smartphone alerts for bill payments and savings goals also prevents late payments and ensures financial disciplines remain intact.

A comparative table highlights popular financial tools and their benefits:

| Tool Name | Primary Function | Key Benefit | User Level |

|---|---|---|---|

| Mint | Budgeting and tracking | Expense awareness and control | Beginner to Intermediate |

| Personal Capital | Investment tracking | Portfolio and net worth analysis | Intermediate to Advanced |

| Credit Karma | Credit monitoring | Free credit score updates and alerts | Beginner |

| Acorns | Micro-investing | Round-up savings and automated investing | Beginner |

By incorporating technology into daily routines, users can create a seamless experience that supports healthy financial habits without adding complexity.

Future Perspectives: Sustaining and Adapting Financial Habits

As financial landscapes and personal circumstances evolve, sustaining healthy habits requires adaptability and forward thinking. The future of personal finance will likely involve greater integration of artificial intelligence and personalized financial coaching, enabling individuals to adjust habits dynamically based on real-time data.

Moreover, with economic uncertainties such as inflation rates fluctuating and unpredictable job markets, building resilient habits—such as maintaining a liquid emergency fund and regularly revisiting financial goals—will be more essential than ever. According to a 2024 report from the World Economic Forum, 68% of individuals who adapt their financial habits in response to changing economic conditions maintain higher levels of financial well-being.

Promoting lifelong habit evolution means regularly revisiting financial routines, learning new skills, and leveraging emerging tools to stay ahead. Public and private initiatives focusing on financial wellness programs are also expanding, helping more people develop and maintain these healthy behaviors.

On an individual level, committing to an annual financial check-up, setting progressive goals, and remaining financially informed will be critical to navigating the complex financial environment of the future successfully.