Personal Finance for Couples: How to Manage Money Together

Managing personal finance as a couple can be both rewarding and challenging. Money plays a significant role in a relationship, influencing everything from daily decisions to long-term goals. According to a 2022 survey by the National Endowment for Financial Education, 35% of couples reported that money disagreements were a leading cause of conflict. However, when approached correctly, financial management can strengthen a partnership and provide a solid foundation for future growth.

Money management is a shared journey that requires transparent communication, mutual respect, and strategic planning. This comprehensive guide will explore actionable ways couples can successfully merge their financial lives, offering practical examples and data-driven insights to help achieve harmony around finances.

Understanding Your Financial Landscape Together

The first step for couples managing money is to gain a clear and complete understanding of each other’s financial status. This includes income, expenses, debts, and assets. Without this transparency, efficient money management becomes difficult.

Start by individually listing all sources of income, monthly expenses, debts, and savings. For example, one partner might have a student loan debt of $25,000, while the other has no debt but a smaller income. Being honest about these details can help avoid surprises later and set the foundation for trust. According to a 2023 Fidelity study, couples who openly discuss finances early in their relationship have a 50% lower risk of future financial disputes.

Anúncios

Tracking all expenses for a month using apps like Mint or YNAB can give an objective picture of spending habits. Couples should then compare notes to identify overlapping expenses (e.g., rent, utilities) and discretionary spending that can be optimized. One real-life case involved a couple in their 30s discovering they each spent $150 monthly on separate streaming services. By consolidating to one plan at $20 monthly, they freed up over $1500 annually for savings.

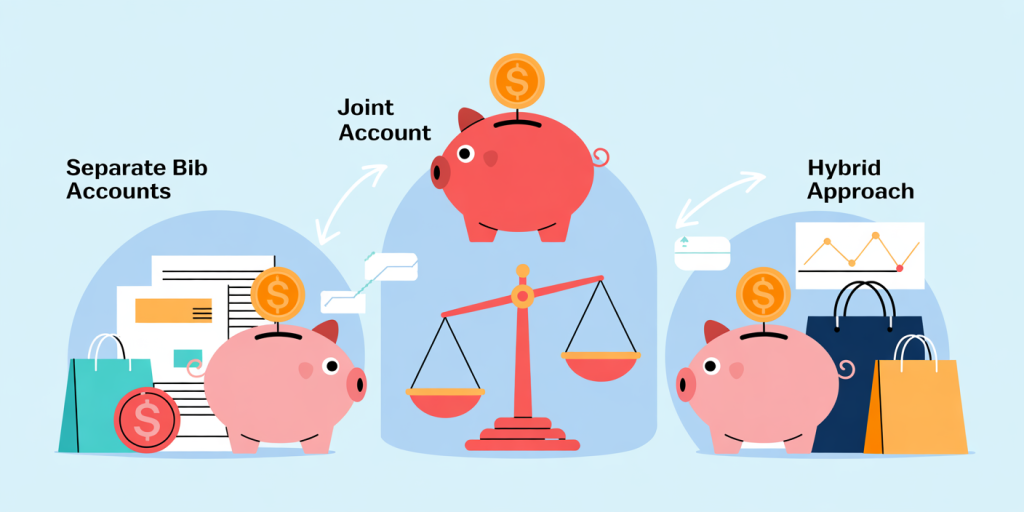

Choosing a Joint or Separate Account Strategy

One of the most debated topics among couples is whether to combine finances or maintain separate accounts. Each approach has pros and cons, and the best option depends on individual preferences and financial situations.

| Account Strategy | Advantages | Disadvantages | Suitable For |

|---|---|---|---|

| Joint Accounts | Simplifies bill payments and budgeting; promotes trust | Can reduce financial independence; risk if one partner mismanages funds | Couples with shared expenses, strong trust |

| Separate Accounts | Maintains financial autonomy; avoids conflicts over spending | Can complicate bill payments and savings goals | Couples valuing independence, uneven incomes |

| Hybrid Approach | Combines joint account for shared expenses and separate accounts for personal spending | Requires good communication; slightly more complex management | Most couples, especially with mixed financial habits |

For example, Lisa and Mark, a couple from Austin, use a hybrid system where they pool 60% of their incomes into a joint account for rent, groceries, and utilities, while each retains separate accounts for personal hobbies and expenses. This balance allows them to collaborate financially without feeling deprived of autonomy.

Anúncios

The key takeaway is that there is no universal “best” method; success comes from aligning the chosen strategy with mutual agreement and clarity.

Establishing Shared Financial Goals

Setting common financial goals can unify a couple’s efforts and foster motivation. Common goals include buying a home, creating an emergency fund, saving for children’s education, or planning for retirement.

It’s essential for couples to prioritize these goals together and create a timeline with specific milestones. For instance, Anna and James wanted to save for a down payment on their first house totaling $40,000 within three years. They calculated needing to save approximately $1120 monthly. By automating transfers from their joint account and cutting discretionary expenses like dining out twice a week, they reached their target on schedule.

Data from a 2022 Bankrate survey shows that 70% of couples who set joint financial goals report higher satisfaction in their relationship. Task sharing also optimizes efforts—one partner could manage budgeting apps while the other handles bill payments.

Remember to periodically review goals to adjust for life changes, such as job changes, birth of a child, or unexpected expenses.

Budgeting Techniques Tailored for Couples

Budgeting is crucial for managing combined incomes and expenses. However, couples often encounter challenges when one partner prefers strict budgeting while the other is more flexible with money.

A practical and widely used approach is the 50/30/20 rule adapted for couples: 50% of income towards necessities, 30% for wants, and 20% for savings or debt repayment. Another technique is zero-based budgeting, where every dollar earned is assigned a specific function, ensuring nothing is left unaccounted for.

An effective example comes from Rachel and Tom, who used a shared Google Sheet to track their monthly expenses and incomes. Every Saturday, they would update their spending to categorize items and discuss whether to adjust or maintain their current spending levels. Using this collaborative budgeting preserved transparency and reduced recurring arguments assessed in a 2023 survey by the Couples Finance Institute, which found collaborative budgeting reduces money conflicts by 40%.

In contrast, an extreme budget might lead to resentment if one partner feels restricted. To counterbalance, allocate a “fun fund” or personal allowance within the budget, preserving a sense of autonomy.

Debt Management Strategies for Couples

Debt—whether from credit cards, student loans, or mortgages—introduces stress into relationships but can be tackled effectively by a united front.

According to the Federal Reserve, as of 2023, the average U.S. household debt stands at nearly $150,000, including mortgages and other loans. For couples, proactively managing debt requires joint prioritization and realistic payoff plans.

One strategy involves the debt snowball method, where the smaller debts are paid off first to build momentum, or the debt avalanche method, which targets high-interest debts first to minimize total interest. Couples should agree on which method to use and budget monthly payment amounts accordingly.

Consider the case of Sylvia and Eric, who faced $60,000 in combined debt. They agreed to the avalanche method, focusing on Sylvia’s 18% credit card debt before addressing Eric’s student loans. They allocated $1500 monthly toward repayments, cutting dining out and subscription costs. After 3 years, they were free from high-interest debt and began directing funds to savings.

Being supportive rather than judgmental is crucial, as financial strain can exacerbate relationship tension.

Planning for the Future: Retirement and Investments

Couples must plan for long-term financial security, which includes retirement and investments. According to a 2024 report by the Employee Benefit Research Institute, 43% of married couples have saved less than $100,000 for retirement, underscoring the need for early planning.

Start discussions about the preferred retirement lifestyle and the expected costs involved. Use online retirement calculators to estimate how much needs to be saved monthly to reach those goals. For example, if a couple wants to retire comfortably at age 65 with $1 million saved, starting at age 30, they need to save approximately $800/month, assuming an average 6% return on investments.

Couples should explore employer-sponsored plans like 401(k)s, IRAs, or joint investment accounts. Diversifying investments between stocks, bonds, and mutual funds enhances security.

For example, Megan and Josh max out their 401(k) contributions, contribute to an IRA, and maintain a joint brokerage account to invest in low-cost index funds. This multi-pronged approach has enabled them to grow their nest egg steadily while balancing risk.

Transparent discussions about risk tolerance and investment values prevent misunderstandings.

Future Perspectives: Adapting Financial Management as Life Evolves

As couples navigate life changes such as marriage, parenthood, career shifts, or relocation, their financial management strategies must adapt accordingly.

Emerging trends highlight the increasing use of technology in managing joint finances. Fintech apps tailored for couples, like Honeydue or Merge, offer tools to share budgeting, bills, and goals in real-time, enhancing collaboration and reducing administrative friction.

Furthermore, societal shifts such as gender income equality and dual-career households demand more flexible money management strategies. According to Pew Research Center, dual-income couples rose to 58% in 2023, emphasizing the need for shared financial literacy and responsibility.

Looking further, financial education workshops for couples, often offered by credit unions or community organizations, are gaining popularity to mitigate conflicts stemming from money mismanagement.

Couples should also consider creating estate plans and wills early, especially if they have children or significant assets, to ensure their financial wishes are respected.

The future of personal finance for couples lies in continuous communication, leveraging technology, and adapting to changing circumstances with a shared vision. The ability to evolve together financially is crucial, as it builds resilience against unexpected financial shocks and reinforces relational bonds.