How to Legally Reduce Your Taxable Income With Smart Investing

Reducing taxable income is a key financial goal for many investors aiming to build wealth efficiently. While taxes are unavoidable, strategic investment decisions can significantly minimize what you owe to the government and maximize your after-tax returns. Importantly, these strategies are entirely lawful and involve understanding tax codes, investment vehicles, and timing. This article explores actionable, practical ways to reduce your taxable income through smart investing, illuminated with real-life examples, data, and comparative insights.

The Relationship Between Investing and Taxable Income

Understanding how investments influence taxable income is foundational before diving into tactics for reduction. Taxable income is your gross income adjusted for deductions and exemptions, which determines the amount of tax owed. Investments generate income in different forms: dividends, interest, and capital gains, all potentially taxable but often at distinct rates. Knowing these nuances enables investors to choose vehicles and strategies that optimize tax efficiency.

For instance, qualified dividends and long-term capital gains in the United States are usually taxed at lower rates than ordinary income, with maximum federal rates currently 0%, 15%, or 20% depending on income brackets (IRS, 2024). This preferential tax treatment presents an opportunity for investors to grow wealth with relatively less tax burden if they hold assets for the long term instead of frequent trading. Measures like tax-loss harvesting, utilizing retirement accounts, and investing in tax-advantaged bonds contribute to tax reduction without compromising growth objectives.

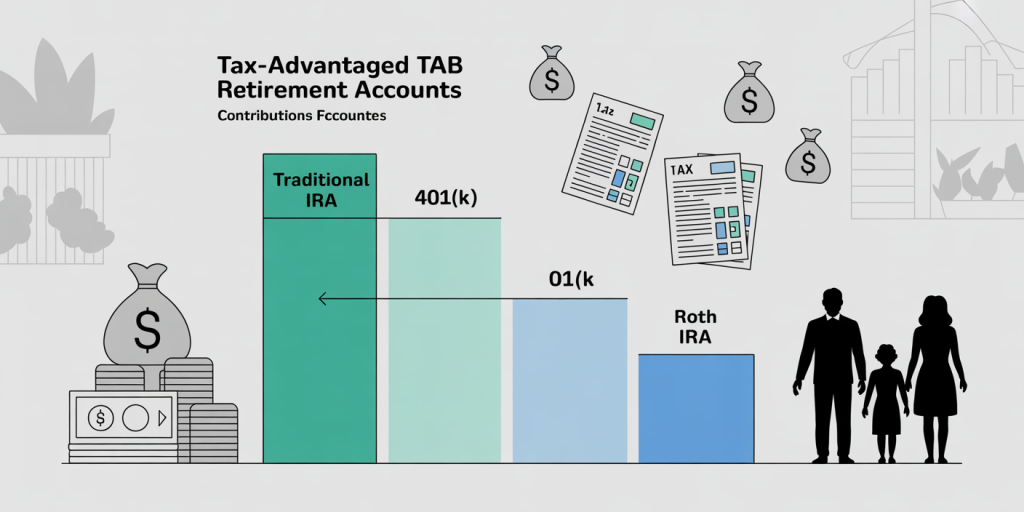

Tax-Advantaged Retirement Accounts: The Cornerstone of Tax Reduction

Anúncios

One of the most straightforward yet underutilized methods to reduce taxable income is investing through tax-advantaged retirement accounts. These include Traditional IRAs, 401(k)s, Roth IRAs, and more specialized vehicles like SEP IRAs for self-employed individuals. Contributions to Traditional IRAs and 401(k)s are generally tax-deductible, directly lowering your taxable income in the year you invest.

For example, if you earn $80,000 per year and contribute $10,000 to a Traditional 401(k), your taxable income for that year could decrease to $70,000, lowering your overall tax bracket. According to the Employee Benefit Research Institute (2023), about 55% of American workers do not maximize their IRA contributions, missing a significant tax-saving opportunity. Roth accounts operate differently by offering tax-free withdrawals in retirement but do not provide immediate tax deductions, which is a trade-off depending on your current versus future anticipated tax rate.

Anúncios

| Account Type | Contribution Limit (2024) | Tax Treatment on Contributions | Tax Treatment on Withdrawals |

|---|---|---|---|

| Traditional IRA | $6,500 | Tax-deductible (subject to income) | Taxable as ordinary income |

| Roth IRA | $6,500 | After-tax contributions | Tax-free |

| 401(k) | $23,000 | Tax-deductible contributions | Taxable as ordinary income |

| SEP IRA (self-employed) | 25% of compensation up to $66,000 | Tax-deductible | Taxable as ordinary income |

Maximizing contributions to these accounts requires planning, especially when balancing immediate tax reduction with long-term investment gains. Many employers offer matching 401(k) contributions, which not only augment retirement savings but can indirectly enhance your tax efficiency by encouraging greater deferrals.

Tax-Loss Harvesting: Turning Losses into Tax Benefits

Tax-loss harvesting is a strategy that enables investors to offset gains by realizing losses on investments strategically. When you sell an investment at a loss, you can use that loss to offset capital gains realized elsewhere, reducing your overall taxable income. If losses exceed gains, you can deduct up to $3,000 from ordinary income per year, carrying forward excess losses to future years.

Consider the case of Jane, who sold stocks with $10,000 in capital gains but also sold other holdings at a $7,000 loss. Her net capital gain becomes $3,000, taxed at a lower rate than ordinary income. If Jane had no gains that year, she could have used the $7,000 loss to reduce ordinary income, lowering her taxable income and thus potentially her tax liability.

This approach is particularly effective in volatile markets, as investors can strategically realize losses while maintaining their desired market exposure by purchasing similar assets or ETFs, adhering to IRS wash-sale rules. According to a 2022 Morningstar study, investors could improve after-tax returns by 1-2% annually through consistent tax-loss harvesting, a significant boost over time.

Investing in Municipal Bonds for Tax-Free Interest Income

Municipal bonds, or “munis,” are debt securities issued by state and local governments with interest payments typically exempt from federal income tax and sometimes state taxes if you reside in the issuing state. This tax advantage makes them attractive for investors in higher tax brackets seeking steady, tax-efficient income.

For example, suppose an investor in the 35% federal tax bracket earns $5,000 interest annually from a taxable corporate bond. After taxes, this income is effectively reduced to $3,250. In contrast, $5,000 in municipal bond interest is often fully exempt, equating to higher “after-tax” income. According to the Securities Industry and Financial Markets Association (SIFMA), the total muni bond market in the U.S. is over $4 trillion, highlighting its prominence.

| Investment Type | Nominal Interest Rate | Tax Rate on Interest | After-Tax Yield for 35% Bracket |

|---|---|---|---|

| Corporate Bond | 4.5% | Ordinary Income Tax (35%) | 2.925% |

| Municipal Bond | 3.5% | Federal Tax Exempt | 3.5% |

While muni bonds generally offer lower yields compared to taxable bonds, their tax-exempt status offers higher effective yields for investors in top tax brackets. This tradeoff suits conservative investors prioritizing income with tax efficiency.

Real Estate Investing: Leveraging Depreciation and 1031 Exchanges

Real estate investments present unique opportunities to reduce taxable income through depreciation deductions and capital gains deferral. Depreciation allows investors to treat property wear and tear as an expense, reducing taxable rental income even if the property appreciates in value.

Take the case of Robert, who owns a rental property generating $20,000 net rental income annually. After claiming $15,000 in depreciation expenses on the property’s structure, Robert reports only $5,000 in taxable rental income instead of the full $20,000, substantially lowering his tax burden. Meanwhile, the property’s market value may rise, building wealth untaxed until sale.

Further tax deferral can be achieved through a 1031 exchange, where proceeds from the sale of an investment property are reinvested in a like-kind property, postponing capital gains taxes. This tool, favored by real estate investors, promotes portfolio growth by deferring tax liabilities.

| Tax Strategy | Benefit | Example |

|---|---|---|

| Depreciation | Reduces taxable rental income | $15,000 deduction against $20,000 rent |

| 1031 Exchange | Defers capital gains taxes on property sales | Sell $500,000 property, reinvest to defer tax |

These strategies require careful tax planning and compliance but can effectively transform taxable income profiles for real estate investors.

Diversifying With Tax-Efficient Funds and ETFs

Not all mutual funds and ETFs are created equal concerning tax efficiency. Actively managed funds tend to generate more taxable events due to frequent trades, while index funds and ETFs typically have lower turnover, resulting in less taxable capital gains distribution. Choosing the right fund structure can thus reduce annual tax liabilities.

To illustrate, Vanguard’s Total Stock Market ETF (VTI), known for its broad diversification and passive management, distributes significantly fewer capital gains than many actively managed equity funds. For taxable accounts, this limitation of taxable events can preserve more investor capital.

A 2023 analysis by Morningstar found that the average annual capital gains distribution for active equity funds was approximately 2%, while passive ETFs showed distributions closer to 0.3%. Investors looking to minimize taxable income from distributions often favor tax-managed funds or ETFs specifically designed to reduce taxable capital gains.

Comparative Table: Capital Gains Distribution (% of NAV)

| Fund Type | Average Annual Capital Gains Distribution |

|---|---|

| Actively Managed Equity | 2.0% |

| Passive ETF | 0.3% |

| Tax-Managed Fund | 0.1% |

Smart investors can balance their portfolio by allocating taxable accounts toward tax-efficient funds while keeping less tax-sensitive holdings in tax-advantaged accounts.

Future Perspectives: The Evolving Tax Landscape and Smart Investing

Tax laws and investment vehicles continue to evolve, making it imperative for investors to stay informed and adaptable. Current trends suggest increasing scrutiny on capital gains taxes and possible changes in retirement account regulations. For example, discussions around increasing capital gains rates for high earners could impact the relative attractiveness of long-term holdings.

Technology and data analytics are increasingly facilitating personalized tax strategies, enabling investors to optimize their portfolios dynamically. Robo-advisors and tax software now offer integrated tax-loss harvesting and account allocation features, maximizing tax benefits year-round.

Environmental, Social, and Governance (ESG) investing is also gaining traction, with potential tax incentives for green investments pending in some jurisdictions. In addition, cryptocurrency investments present new frontiers with unique tax implications and opportunities for structuring.

In light of these trends, partnering with financial advisors and tax professionals remains essential to navigate complexities and seize emerging opportunities for tax-efficient investing. Consistent education, strategic planning, and flexibility will remain the cornerstones of legally reducing taxable income through smart investing.

By incorporating tax-advantaged accounts, applying tax-loss harvesting strategies, investing in municipal bonds, utilizing real estate tax benefits, and selecting tax-efficient funds, investors can effectively lower their taxable income while building wealth. This multi-faceted approach, backed by data and real-world examples, empowers investors to keep more of their earnings and achieve financial goals with compliance and confidence.